Last Sunday, JL Collins put out a post that explains his decision to change this asset allocation.

I have deep respect for JL Collins.

As an avid reader of financial independence content, I have followed his blog for sometime. He started writing as a way to archive and communicate all these money and life lessons for his daughter.

His The Simple Path to Wealth is a good book if you wish to learn about the twin topic of index investing and financial independence.

JL explains the following in his blog post:

- His preferred personal investment allocation is in pre-dominantly United States not having an International allocation.

- His advise to a person like his daughter, a US person, is that you just stick with a Vanguard Total Stock Market Index Fund, not an ETF, but also a US fund because there is no need for international diversification.

- For international investors like you and me, his recommendation is something like Vanguard’s Total World Stock Index Fund or the ETF version VT, which covers US, International, and Emerging Markets.

- He has decided to re-allocate his money in IRA accounts from the mutual fund VTSAX to the ETF VT, avoiding it being a taxable event and thus avoiding capital gains tax. He won’t change the rest of his net wealth that is in other accounts because he would have to pay capital gains taxes.

JL explains his shift in thinking:

I try hard to avoid politics on this blog, and I could be wrong, but in short here’s my take:

The economic policies of this administration have me concerned.

Tariffs, and especially the erratic implementation of them, are teaching our allies and enemies alike that the US is no longer a reliable trading partner. In response they are turning to each other to form new and stronger trading bonds and to diminish the dominance of the US on the world stage. These tariffs are also likely to be very inflationary once companies are no longer willing or/and able to absorb them.

The US dollar has been the world reserve currency since the end of World War II, but more and more other countries are seeking to trade in other currencies. Many would dearly love to displace the dollar as that reserve currency, just as the dollar replaced the British Pound after WWII. We are fortunate that now, unlike then, there is no obvious, viable alternative. So far.

Last year the dollar dropped in value against other currencies by ~10%, the largest drop in 50 years. Oh, and there is that pesky little issue of our debt, currently soaring toward 40 Trillion Dollars ($40,000,000,000,000).

2025 was an exceedingly robust year for stocks worldwide. The US as measured by the S&P 500 returned 16.4%. The average over the last 50 years has been ~12% making this exceedingly strong return. As long as you don’t look at the rest of the world that is.

Of the 30 top performing countries, the worst performer was still up ~11%. That was India. Second worst, the US with that 16.4%.

Most of Europe was over 30% and not a single EU country was less than 20%. China returned ~30%, as did Canada. Mexico came in at only #10 on the list, good for ~55%. Against this backdrop, 16.4% is embarrassing.

For these reasons, I see that declining trend of the US share of the world economy described above accelerating.

I have mixed feelings when I read this.

I have no problems with the eventual recommendation to be more internationally diversified. That is what i tell you the readers. That is how we setup our client’s portfolios at Providend as well.

I guess I felt that… what JL raised is not new.

- If the conviction to adopt a systematic passive strategy like index investing, to stay and invested in a basket of diversified US equities

- comes from reviewing a long history of market returns,

- which are market returns that happen during periods where many of the pivotal events that JL Collins mentions that would caused him to shift his views,

- then does that mean his original personal recommendation, his recommendation to US investors is flawed enough?

Market Returns do Come with Shifts in Geopolitics

Sometimes I wonder if it is because international market returns look better now and it makes people more comfortable to invest.

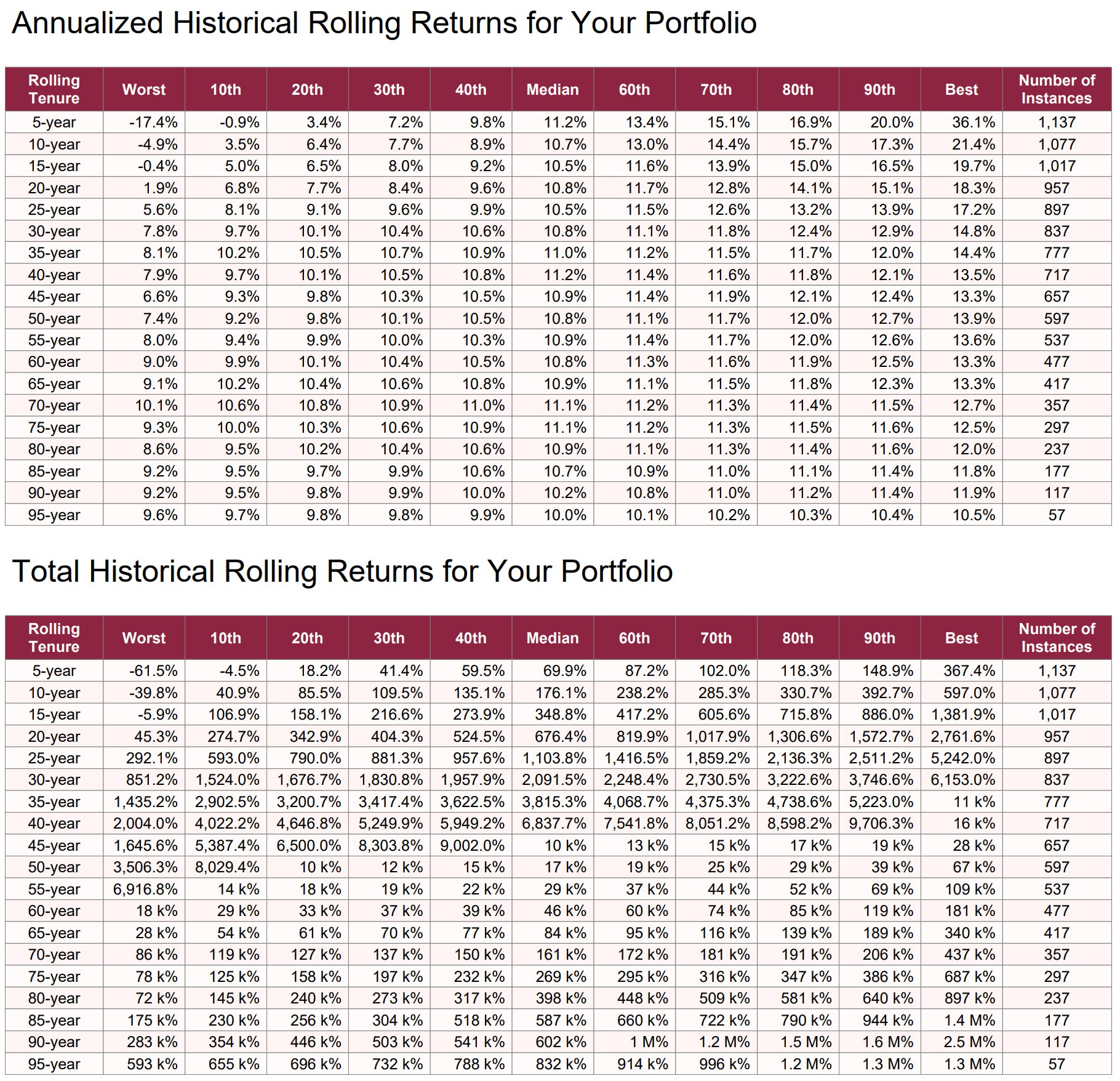

One of the reasons a data-focused person will have higher conviction in buying-and-holding a 100% US region is the long history of market data.

I used Gilgamesh to generate the rolling x-years return for the US large cap, the S&P 500 with data from 1926 to 2025:

You can observe that short term of less than 20-years, you can have a challenging outcome if you are unlucky, but generally it is pretty optimistic.

The most important thing is that USD has severely weakened in some of these timeframe. There is also a time frame where Globalization took place in a rather big way. These period considers the periods before World War II and after that.

So does JL mean to tell us his advise to US investors in the past is made considering the good range of returns in the past but not the history of events that comes with the returns?

That is damn odd.

One of the critical reasons we prefer a more regional diversified portfolio for you (readers) and our clients at work is that the evidence of history tell us that there will be geopolitical shifts that may worry some of you in the past two years is not new.

You may feel slightly more at ease if your net wealth is less entrenched in a single factor, region, sector. You won’t get the best return, but if you wobble and sell out of a buy-and-hold strategy, then you don’t get that best return in the first place.

This is a critical feature which prevents us from allocating 100% of your portfolio into Wakanda if the companies of Wakanda comes to dominate the world.

Seemingly Good Advice Can be Made With Narrowed & Flawed Mental Conclusions

As I grew older, I find myself searching for what are the more critical factors to build wealth, provide income that are more evergreen. I fear that the important, high level investment recommendations I would write and make to you is based on my mental conclusions that were too narrow.

- What I wrote about dividend investing or value investing probably helps you if you are wearing the hat of a retail portfolio manager managing dividend stocks.

- What i wrote about investing in REITs probably helps you if you are a retail portfolio manager managing only REITs.

I admit that my conviction about broad things then might be just as narrowed, which lead me to make questionable recommendations to you.

How does this impact you?

You will feel overconfident about what these strategies could do. You may feel that when situations changed, you cannot invest in REITs, stocks that provide high dividends anymore.

Which is why I have deeper thoughts about what JL Collins wrote because it made me question if my current understanding of investment strategies is incomplete yet, that it is still flawed.

I guess I might be too harsh on myself, and perhaps on JL Collins. We are not professionals, we meaningfully want the best for our readers, and put out what we know about our experiences.

In a way, you should judge or question if the person you listen to has a well-formed view of the world.

I am super critical about people bringing up investment opinions that they hear in the media because most are not aware of the time-frame of investment the person in the media is referring to. Most of the people in the media has a time-frame of investment of one year or less and your time-frame of investment is more than that, so does it matter?

This difference in time frame is critical and you end up scaring yourself for no reason.

If I am not being clear:

- My conviction in preferring you to have a either systematic-active, or systematic-passive, broadly sector, and region diversified, low cost portfolio strategy to build wealth is based not just on the market returns in the past but also that there exist good times, poor times, of USD depreciation.

- My conviction in using and preferring you to use a Safe Withdrawal Rate Framework to size up how much you need in income planning also includes good times, and poor times like this.

Geopolitics like the recent past is not new. You may just forget about it during another part of your life or that you weren’t investing then. It is always around.

Credit to JL Collins for coming out to say this.

It is not easy when you are popular, in a position to provide strong conviction and decide to tell people that you need to change.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.